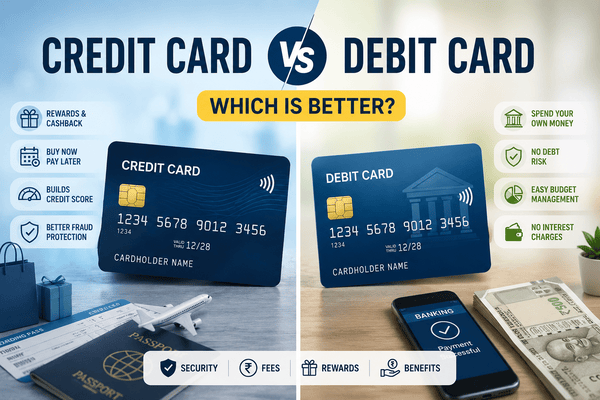

Introduction

In today’s digital world, cards have become an essential part of our financial lives. Whether you’re shopping online, booking tickets, paying bills, or making purchases at stores, you have likely used either a credit card or a debit card. While both cards may look similar and perform many of the same functions, they work very differently behind the scenes.

Many people often ask, “Should I use a credit card or a debit card?” The answer depends on your financial goals, spending habits, and ability to manage money responsibly.

A debit card allows you to spend money directly from your bank account, while a credit card lets you borrow money from the bank up to a certain limit and repay it later. Understanding the advantages and disadvantages of both can help you make smarter financial decisions.

In this detailed guide, we’ll compare credit cards and debit cards across various factors including rewards, security, spending control, credit score impact, fees, and more.

What is a Debit Card?

A debit card is a payment card linked directly to your savings or current bank account. Whenever you make a purchase, the amount is immediately deducted from your account balance.

How Debit Cards Work

- You swipe, tap, or enter your card details.

- The bank verifies available balance.

- The amount is deducted instantly from your account.

- The transaction is completed.

Key Features of Debit Cards

- Direct access to your bank account.

- No borrowing involved.

- Easy cash withdrawal from ATMs.

- Usually issued free with bank accounts.

- Helps control overspending.

Advantages of Debit Cards

1. No Debt Risk

Since you spend only the money available in your account, there is no risk of accumulating debt.

2. Easy Budget Management

Debit cards help maintain financial discipline because every transaction reduces your available balance immediately.

3. No Interest Charges

You never pay interest because you are using your own money.

4. Easy Approval

Almost anyone with a bank account can get a debit card.

5. Lower Fees

Most debit cards have minimal annual fees compared to premium credit cards.

Disadvantages of Debit Cards

- Limited rewards and cashback.

- No credit score improvement.

- Lower fraud protection in some cases.

- Cannot build credit history.

- Limited purchase protection benefits.

What is a Credit Card?

A credit card allows you to borrow money from the card issuer up to a pre-approved credit limit. You can make purchases now and repay the amount later.

How Credit Cards Work

- Bank assigns a credit limit.

- You make purchases using borrowed money.

- A monthly statement is generated.

- You repay the amount before the due date.

- If not paid fully, interest is charged on the outstanding balance.

Key Features of Credit Cards

- Buy now, pay later.

- Credit limit provided by the bank.

- Interest-free period (typically 20-50 days).

- Reward points and cashback.

- Builds credit history.

Advantages of Credit Cards

1. Build Your Credit Score

Responsible usage helps improve your CIBIL score and credit profile.

2. Earn Rewards and Cashback

Most credit cards offer:

- Cashback

- Reward points

- Travel benefits

- Airport lounge access

- Fuel surcharge waivers

3. Better Fraud Protection

Many banks offer zero-liability protection for unauthorized transactions if reported promptly.

4. Emergency Financial Support

Credit cards provide instant access to funds during emergencies.

5. EMI Conversion

Large purchases can often be converted into affordable monthly installments.

6. Travel Benefits

Premium cards offer:

- Airport lounge access

- Travel insurance

- Hotel discounts

- Flight offers

Disadvantages of Credit Cards

1. High Interest Rates

Interest rates can range from 24% to 48% annually if bills are not paid on time.

2. Risk of Overspending

Easy access to credit can encourage unnecessary purchases.

3. Late Payment Charges

Missing payments can lead to:

- Late fees

- Interest charges

- Lower credit score

4. Annual Fees

Some premium cards charge annual or renewal fees.

Credit Card vs Debit Card: Detailed Comparison

| Feature | Credit Card | Debit Card |

|---|---|---|

| Source of Funds | Borrowed from Bank | Your Own Money |

| Credit Score Impact | Yes | No |

| Interest Charges | Applicable if unpaid | None |

| Rewards & Cashback | High | Limited |

| ATM Withdrawal | Cash Advance Charges | Usually Free/Limited Charges |

| Spending Control | Lower | Better |

| Debt Risk | High | None |

| Emergency Usage | Excellent | Limited to Balance |

| EMI Facility | Available | Rare |

| Approval Process | Credit Check Required | Easy |

Which Card is Safer?

Both cards use modern security features such as:

- EMV chip technology

- OTP verification

- Contactless payments

- Mobile banking controls

However, credit cards generally provide stronger fraud protection because the disputed money belongs to the bank until resolved.

Winner: Credit Card

Which Card Helps Build Credit Score?

Only credit cards contribute to your credit history and CIBIL score.

Good credit card habits include:

- Paying bills on time.

- Keeping credit utilization below 30%.

- Avoiding unnecessary loans.

Winner: Credit Card

Which Card is Better for Online Shopping?

Credit cards are often preferred because they offer:

- Higher cashback.

- Reward points.

- Purchase protection.

- Extended warranties.

- Fraud protection.

Winner: Credit Card

Which Card is Better for Beginners?

For students and first-time users:

- Debit cards teach financial discipline.

- No debt risk.

- Easy to manage.

Winner: Debit Card

Which Card is Better for Frequent Travelers?

Travelers can benefit from:

- Airport lounge access.

- Travel insurance.

- Flight rewards.

- Hotel discounts.

Winner: Credit Card

When Should You Use a Debit Card?

Use a debit card if:

- You want strict spending control.

- You are new to banking.

- You prefer avoiding debt.

- You don’t need rewards or credit building.

When Should You Use a Credit Card?

Use a credit card if:

- You can pay bills in full every month.

- You want cashback and rewards.

- You travel frequently.

- You want to build a strong credit score.

Expert Recommendation

The smartest financial strategy is not choosing one card over the other—it is using both wisely.

Use your debit card for:

- Daily expenses

- ATM withdrawals

- Budget management

Use your credit card for:

- Online shopping

- Travel bookings

- Utility payments

- Reward-generating purchases

Always pay your credit card bill in full before the due date to avoid interest charges.

Frequently Asked Questions (FAQs)

Is a credit card better than a debit card?

A credit card offers rewards, credit score benefits, and stronger fraud protection, while a debit card provides better spending control and no debt risk.

Can I build my CIBIL score with a debit card?

No. Debit card usage does not affect your credit score.

Is it safe to use a credit card online?

Yes, credit cards generally offer better fraud protection and chargeback facilities.

Should students use credit cards?

Students should start with debit cards. If financially disciplined, they can later consider beginner-friendly credit cards.

Which card is best for online shopping?

Credit cards usually provide better cashback, rewards, and purchase protection benefits.

Conclusion

If your goal is financial discipline, choose a debit card.

If your goal is rewards, credit building, and additional benefits, choose a credit card.

For most financially responsible individuals, using both cards strategically offers the best combination of convenience, security, rewards, and financial growth.